Beyond the Boom: India's Economic Recovery at a Crossroads

- Paras Jasrai

India’s economic recovery post the pandemic has been defying expectations. The GDP growth has averaged above 7% since FY22. This has come at a time when there have been plenty of geopolitical rifts around the globe in the aftermath of the COVID-19 pandemic, making India’s recovery process even more praiseworthy. Does that mean that all is well so far as the Indian economy is concerned? If so, are we on the golden path of clocking 7% growth year after year?

Unpacking India's Consumption Conundrum

Consumption is the centrifugal force around which India’s economy majorly revolves around. Private final consumption expenditure (PFCE) is taken as a proxy for tracking trends in consumption demand for the broader economy. It represents over 60% of India’s GDP. A higher consumption growth results in higher demand for goods and services which further fuels investment demand in the economy and thus the GDP growth. But what’s startling is the yawning difference between the GDP and PFCE growth in FY24.

Long-term trends in the growth of GDP and PFCE suggest that consumption demand has been the driving force of GDP growth in India (see Figure 1). There have been years where other driving factors were behind the GDP growth. One such year has been FY24. The PFCE growth stood at a meagre 3.0% in FY24 which was the slowest since FY03 (barring the COVID-19 impact in FY21). As a result, the wedge between the growth in GDP and PFCE stands at 4.6 percentage points (pp) which is the highest since FY1952. Such a large difference at a time when the economy is roaring appears to be perplexing.

Figure 1:

So what explains the collapse in PFCE growth?

The slowdown in the PFCE growth can be attributed to multiple reasons.

Firstly, inflation.

Inflation in India like the world at large had been touching multi-year highs since late FY22 and stayed above the 6% in FY23. The triggering factor behind the inflation was the surge in food prices. Food remains the biggest item in household budgets (despite its falling share over the years) and thus high food inflation meant lower spending toward non-discretionary items. High inflation shaves off the purchasing power of households; especially pinching the lower income bracket households.

Second, climate change.

Extremities in weather patterns have been increasing over the years primarily due to climate change. This has been affecting the agricultural sector which remains at the vagaries of the weather despite the progress in irrigation intensity in various parts of the country. Lower-than-normal rains in the 2023 monsoon season owing to the progression of El Nino impacted the crop productivity and thereby the agricultural output in FY24. The agriculture sector is estimated to record a paltry growth of 0.7% in FY24, at an eight-year low. This holds primacy given that nearly 45% of India’s labour force still depends on this sector for livelihood. Thus, impacting rural demand.

Thirdly, K-POPulation.

The demand recovery post-pandemic is K-shaped whereby the economic position of upper-income households has recovered handsomely while that of the lower-income ones still has a catch-up to play. This is borne out from various data points such as the phenomenal sales of luxury residential homes, passenger vehicles, high-end mobile phones, etc. On the other hand, the sales of low-end smartphones, affordable houses, and two-wheelers have been lagging and some are yet to even reach the pre-pandemic level.

The NSO recently released a detailed picture of PFCE capturing the trends in consumption items by purposes and by durability till FY23. A glance at the data indicates that demand for durable goods and services clocked a strong growth of 14.4% and 8.8%, while that of semi-durables and non-durables was down to negative 3.1% and 6.3% respectively in FY23 from the previous year. The PFCE growth in FY23 was 6.8%, led by services and durable goods. These items are consumed in a larger proportion by the upper-income brackets further accentuating the K. At a time when the PFCE growth has slipped to 3% in FY24, with the services sector growth pegged at above 7% and this coupled with a weak rural demand (agriculture growth), the trend appears to have sustained even this year.

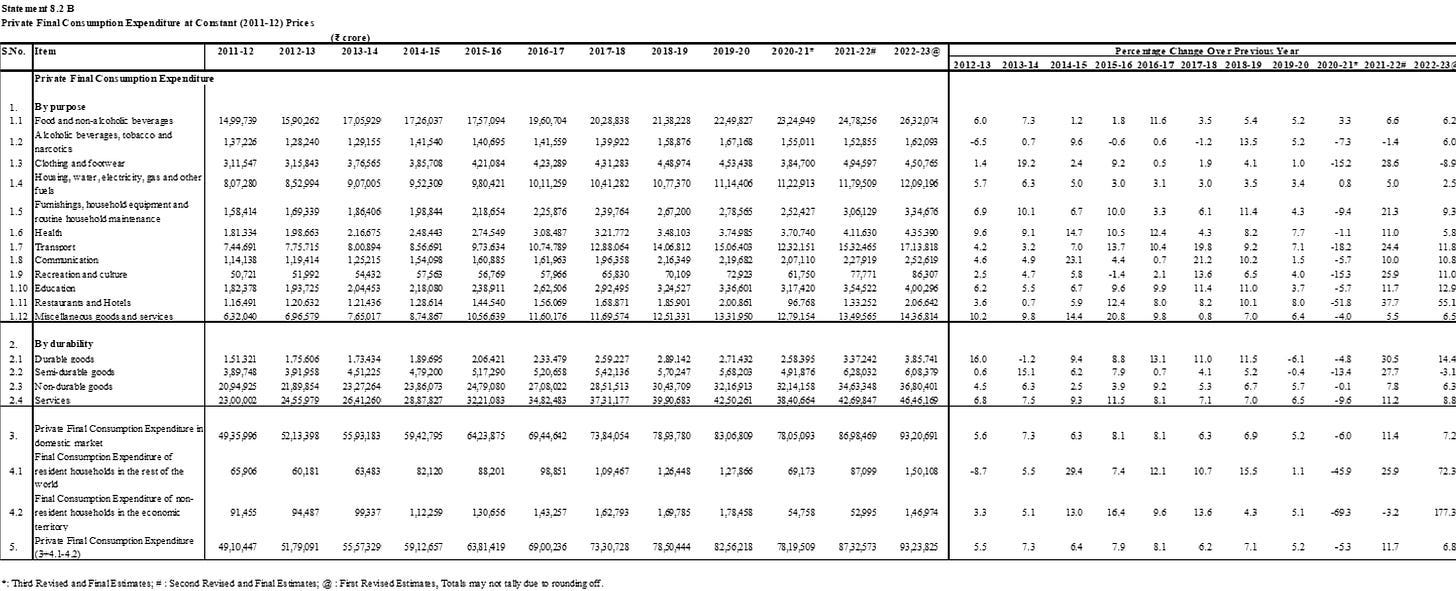

Figure 2:

Source: Press Release of NSO dated 29 February 2024.

Lastly and perhaps more importantly, real wages.

Households are more confident of their consumption when they face better prospects with their incomes. The periodic labour force gives the nominal wages/earnings data for regular salaried and self-employed persons which is available from July-September 2017 till April-June 2023. This has been deflated to get the trend in real wages. A closer look at the data points out that, although there has been some modest improvement in real wages of salaried persons (see Figure 3), it trails short of the pre-pandemic period. Likewise, this has been the case for the gross earnings of self-employed workers (see Figure 4).

This becomes important once one considers that the consumption demand witnessed a slack before the pandemic. The PFCE growth stood at a decadal low of 5.2% in FY20 due to the spiraling impact of various shocks such as demonetisation, GST implementation, etc. Not surprisingly, the GDP growth did suffer as well. It slowed to an 11-year low of 3.9% in FY20. The fall in real wages/earnings of the salaried/self-employed workers was one of the reasons for the same.

Figure 3:

Figure 4:

Conclusion

While India's economic recovery post-pandemic has been commendable, the significant slowdown in PFCE growth in FY24 underscores the challenges ahead. The factors contributing to this slowdown—ranging from inflation and climate change impacts on agriculture to the K-shaped recovery and stagnant real wages—highlight the multifaceted nature of the issue at hand. However, there is a glimmer of hope on the horizon. With inflation expected to moderate to 4.5% in FY25 (by the RBI) and the potential stabilization of agricultural outputs with the El Nino turning neutral after the summer season, there's an opportunity for real wages to improve, thereby bolstering consumption demand. For India to sustain its growth trajectory and ensure it benefits a broader segment of the population, it's imperative to address these underlying challenges. Strengthening the agricultural sector, supporting wage growth, and fostering a more inclusive recovery are crucial steps toward reigniting the engine of consumption and setting the stage for more resilient and equitable growth in the years to come.

Views are personal.

Nice read. Interested to know if you have any solutions in mind for the " fostering a more inclusive recovery" that you mention in the conclusion.